Saving vs investing: How hard is your money working for you?

Posted On:16th,Oct 2024

Catagory:Personal Finance

As kids, we are told to save, save in our bank account or save in our piggy bank. In reality, I did not know that we should have been investing, instead of just saving. Many think these two are the same, but one will keep you in a loop of saving and stagnation while the other can provide you with financial freedom.

At the end of the day, it comes down to how hard your money is working for you. Your money needs to outpace inflation to ensure you're not getting poorer, by life getting more expensive. After all, inflation is everyone's enemy.

Do you have lazy money workers or highly productive money workers? Let's dive into this head first and figure out how we can make your money work harder.

What is the difference between saving and investing?

For most people, these two are the same thing, and there are many similarities between them. One of the most important similarities is that both are used to save up for some goal. The difference comes in the asset class that your savings is invested in. As the old saying goes, a higher risk is associated with the probability of higher returns.

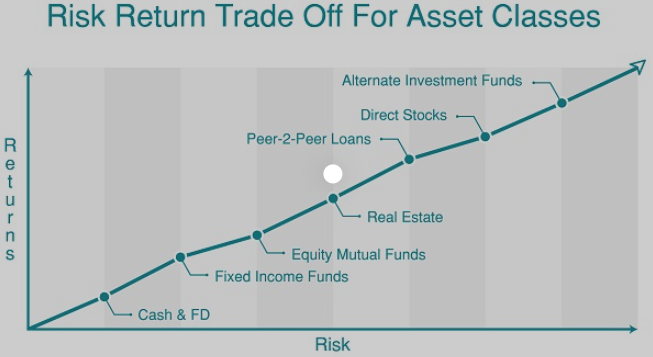

Let's look at the below example from Onemint, showing how different asset classes have the potential for higher returns. As you can see money in the bank is invested in cash only, and that is the point furthest to the left. To make your money work harder, you have to move to the right, but this comes with more risk.

Practical examples of the risk and return investment options in SA

|

Asset class |

Return |

Inflation |

Return after inflation |

|

FNB Bank savings |

4.3% |

4.4% (August 2024) |

-0.1% |

|

Allan Gray Money Market fund |

9.1% (Latest 12-month return) |

4.4% (August 2024) |

+4.7% |

|

Prescient Income Provider fund |

11.14% (Latest 12-month return) |

4.4% (August 2024) |

+6.74% |

|

Fairtree Equity Fund |

12.84% (10 years, annual performance) |

4.4% (August 2024) |

+8.44% |

|

Peregrine High Growth Hedge Fund |

14.04% (10 years, annual performance) |

4.4% (August 2024) |

+9.64% |

As you can see on the graph, moving down, we increase the risk asset class. If you keep your money in the bank you will earn 4.3% over 1 year, at the end of the year, you will be 0.1% poorer as your money did not keep pace with inflation. As you start taking on more risk and investing in riskier asset classes you will notice your return after inflation increases.

Rule of 72 and rule of 114

A simplistic, yet insightful rule to calculate how hard your money is working for you is the rule of 72. The rule of 72 calculates how long it will take for your money to double given a rate of return. Let's use the Fairtree Equity fund as an example. The fund returned 14.04% per year for the last 10 years. Using the rule of 72 we take 72 and divide it by 14.04. The answer is 5.13. This is the number of years it will take to double your money.

You can also use the rule of 114 to calculate how long it will take to triple the value of your money by using the same method used for the rule of 72.

Summary

Saving and investing are not the same, despite having similarities. Investing involves putting money into riskier assets with the potential for higher returns while saving is limited to cash-only assets with lower returns. The risk vs return trade-off can be evaluated using the rule of 72 and rule of 114, which calculate the time it takes to double or triple your money based on the rate of return. It's important to have your money working harder for you to outpace inflation and achieve financial freedom. Now get out there and start investing!

At Finsights, we want you, the everyday hero, to take control of your finances, become aware of financial independence, grow your knowledge, and let us be your financial independence partner.

Onward to Financial Independence